")

As we prepare for COP30 in November 2025, all eyes are on the COP30 Presidency, held by Brazil, which is leading the development of a roadmap to scale climate finance over the next decade. The objective, as agreed at last year’s COP summit in Baku, is to mobilize at least $1.3 trillion annually by 2035 to support climate action in developing countries.

Finance must be sufficient to meet the urgent need for mitigation and to help communities adapt to and cope with the impacts of already baked-in climate change. For many low-income and climate-vulnerable communities, this adaptation finance is a matter of life and death. Current estimates of adaptation needs in developing countries stand at around $300 billion per year – a figure that is rising rapidly as countries, and high-emitting countries in particular, fail to sufficiently reduce emissions and the world veers closer to 2 degrees (or more) of warming. Yet, adaptation is chronically underfunded, with only around 10% of developing countries’ adaptation needs being met through international climate finance.

As negotiators head to Bonn this month for the regular mid-year Climate Meetings, which will be crucial to make progress ahead of COP30, the adaptation finance challenge is daunting. Even prior to the recent and dramatic international aid cuts announced by the US and a number of European governments, many were already pinning their hopes on the private sector to help close the finance gap, and this pressure has only increased. But is this realistic or just wishful thinking?

Enthusiasm for the role of the private sector

From a developed and developing government standpoint, dwindling foreign aid budgets and competing domestic pressures have made it practically and politically expedient to look to the private sector for support. According to the Independent High Level Expert Group on climate finance, “External private finance to EMDCs [Emerging Markets and Developing Countries] other than China at present is only around $30 billion. It can and must reach $450–500 billion by 2030, an increase of 15 to 18 times.” That would require an extraordinary scale-up within a five-year period.

From a corporate perspective, there are financial and strategic incentives to invest in climate resilience – not least avoiding costly disruptions in operations and supply chains or delivering cost savings under a changing climate. There are also new markets emerging for adaptation goods and services. The Global Commission on Adaptation’s flagship report, Adapt Now, estimates that investing $1.8 trillion globally from 2020 to 2030 could generate $7.1 trillion in net benefits.

Nonetheless, significant barriers and limitations to private adaptation finance remain in place. And, the fact remains: if this were easy and profitable, it would be happening already. So, what does the evidence actually tell us?

The evidence base

Research funded by the Zurich Climate Resilience Alliance, to be published in September 2025, quantifies developing countries’ adaptation needs and explores where private sector contributions are realistic, broken down by sector – water or agriculture, for example – and by country type: low- and middle-income countries and small island developing states (SIDS).

What emerges is a highly varied picture.

Take engineered coastal protection, such as sea walls, as an example. These are public goods and, in developing countries, their funding has been delivered almost entirely by the public sector. Trying to scale up private finance investments for them is not a new challenge: there have been attempts to get flood protection off public balance sheets for decades with low success.

In contrast, in sectors like agriculture, there’s much more potential for the private sector, particularly for middle-income countries. This is already seen in blended finance data, where agriculture comprises the largest share of recent deals, and there are numerous examples of innovative technologies and financial models emerging via adaptation accelerators.

The forthcoming report considers all key sectors and, while there are opportunities for the private sector, four critical factors must be addressed.

Four considerations for private adaptation finance

1. Who is really paying for adaptation?

There are opportunities for private financial markets to invest in green bonds, blended finance or public-private partnerships; these can all be profitable for the private sector. Ultimately, however, this is just the financing, providing the upfront costs using a range of different instruments. This is not the same as paying for these costs over the project’s lifetime – a burden which will often ultimately fall to households, either directly or as taxpayers via their governments. There are serious ethical questions if the private sector is profiting while the actual, long-term costs are borne by countries and communities that are suffering from a crisis they did not cause.

2. Bankable projects are in short supply

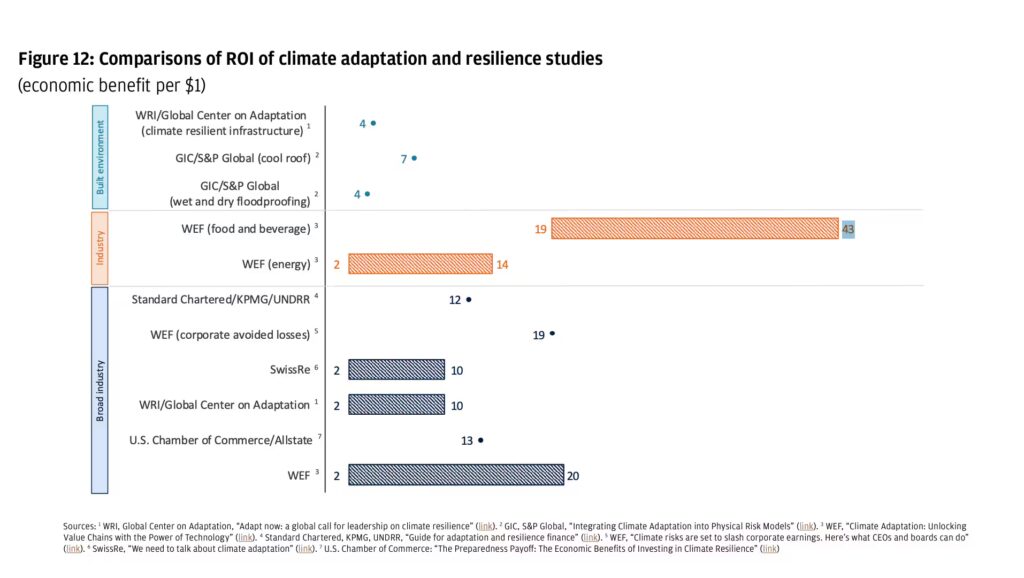

There are many barriers to private sector investment in adaptation, but the most critical is the lack of direct financial returns. There are some very high estimates of returns on investment being put forward. Standard Chartered estimated returns of $12 per dollar spent, for example, and some estimates go as high as $43, as seen in this table taken from JP Morgan’s report, Building resilience through climate adaptation.

These are, however, largely based on overall returns to society – including social and environmental benefits, most of which do not accrue to the private sector investor or generate direct revenue streams; the benefits are often public goods. This is unsurprising. If the return on investment were truly this compelling, wouldn’t we expect the private sector to be doing more – and far faster – already?

3. Technical solutions can only take us so far

In contrast to mitigation – where, for example, solar panels will produce predictable returns everywhere, business models are replicable and scaling is simple – there are far fewer quick-fix and scaleable technical solutions for adaptation. The most effective adaptation solutions are highly context-specific and many involve behavioural change. Thus, to be successful, they must be driven by and adapted to local climate impacts, as well as the needs and vulnerabilities of different groups within the affected communities. They must give communities, including women, youth and Indigenous People, decision-making authority in identifying and implementing solutions. This complexity makes them harder to scale and less attractive for commercial investors, even though giving community members a clear stake in the solution is imperative, for impact and for sustainability.

4. Blended finance is not a silver bullet

It’s now fashionable to say that it’s not about deciding between public or private, but about how to use limited public resources to derisk and incentivize private funds through blended finance. Although often reported as yielding a 1:6 leverage ratio (i.e. $1 of public funding brings in $6 of private funding), real-world data tell a different story. ODI research puts the average at 1:0.75 for all developing countries, falling to 0.37 for Low-Income Countries (LICs); McKinsey & Company argues this could be increased to 1.6; Oil Change International finds 1:0.85 for developing countries, dropping to 0.69 for LICs. Even the pro-blended finance group, Convergence finds it to be 1:1.8. There are also concerns about whether these projects are truly additional – i.e. would the private sector have invested anyway, without public funding? – and aligned with local priorities. This is not to say that blended finance cannot work, but the reality doesn’t live up to the hype.

Is billions to trillions a fantasy?

Ten years ago, the World Bank and other multilateral lenders discussed transforming “billions to trillions” to fund the Sustainable Development Goals, with small amounts of public funding unlocking vast amounts of private financing. But recently, the World Bank President, Ajay Banga, acknowledged that this was “unrealistic” and “bred complacency.” Its chief economist, Indermit Gill, has called the vision a “fantasy”; the climate sector must not fall into the same trap. It’s time to stop wishful thinking. Real progress means facing facts, making serious public investments and overhauling how global finance works — not recycling promises of private capital that never comes.

What comes next?

There is no simple fix for mobilizing more than $300 billion annually for adaptation in developing countries. But these two principles must remain central:

1. In line with the Paris Agreement, developed countries have obligations to provide adaptation finance, as well as the core UNFCCC principle of Common but Differentiated Responsibilities. This legal obligation remains true, even in the current context of restricted aid budgets. Developed countries cannot be let off the hook because this is not easy or convenient. The cost of climate impacts does not simply disappear. It is borne by developing countries and communities.

2. The polluter-pays principle is a widely accepted norm in international and domestic environmental law, with broad international adoption. It should be used to create new sources of public funding, by putting new levies on polluting activities, such as extracting fossil fuels and excessive consumption and air travel.

Developed countries must increase the size of international public finance available for climate action. While there are clearly enormous pressures on public finances, there are ways to increase flows for climate action. This should include:

⦁ Ending harmful fossil fuel subsidies – subsidies currently amount to around $600 billion worldwide.

⦁ Establishing new polluter-pays funding sources that deliver substantial and predictable funds that are less prone to changes in national administrations, including, a fossil fuel extraction levy ($210 billion/year); an air ticket levy ($4 billion to $150 billion/year); and a 2% tax on billionaire wealth ($250 billion/year).

The private sector has a key role to play and in some sectors it will be critical. But it cannot close the adaptation finance gap alone. And efforts to encourage and support private sector engagement must not become a substitute for the public funding wealthy nations are obligated to provide.

This blog was originally published by the World Economic Forum on 10th June 2025. You can read the original here.

Comments